Navigating 2026: 7 Key Themes for Your Retirement Journey

Stock markets are up, but so is anxiety. As we head into 2026, are you worried about "giving back" your gains? From AI and elections to the national debt, here are 7 key themes every retiree needs to ... ...more

Retirement ,Economy Market &Investing

December 09, 2025•5 min read

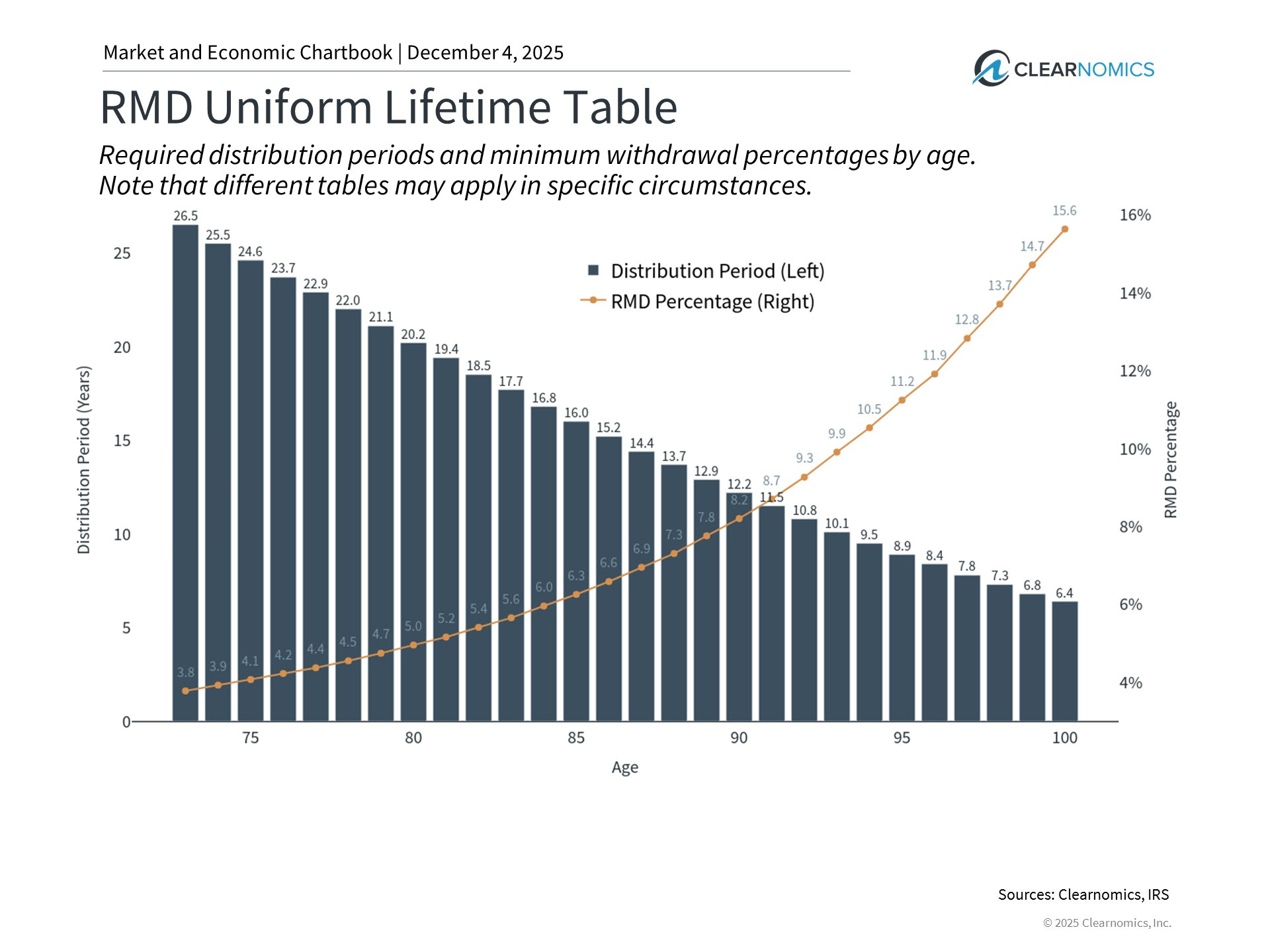

Your Year-End Financial Inspection: 3 Moves to Consider Before December 31

As the year winds down, don't miss the chance to perform a "maintenance check" on your retirement plan. We discuss three critical strategies—RMDs, Roth Conversions, and Tax-Loss Harvesting—that need y... ...more

Tax

December 04, 2025•4 min read

The Ghost in Your Portfolio: How to Spot and Manage Phantom Income

Imagine getting a tax bill for money you never received. It’s called "phantom income," and it can catch even experienced investors off guard. Here is how to spot it and keep your retirement plans secu... ...more

Tax ,Investing

December 03, 2025•3 min read

Medicare’s Hidden Cost: How 2025 Income Impacts Your Wallet in 2027

Did you know the income you earn in 2025 determines your Medicare premiums for 2027? It’s called the IRMAA surcharge, and it can be a nasty surprise. Here is how to manage your income today to avoid p... ...more

Health

November 22, 2025•3 min read

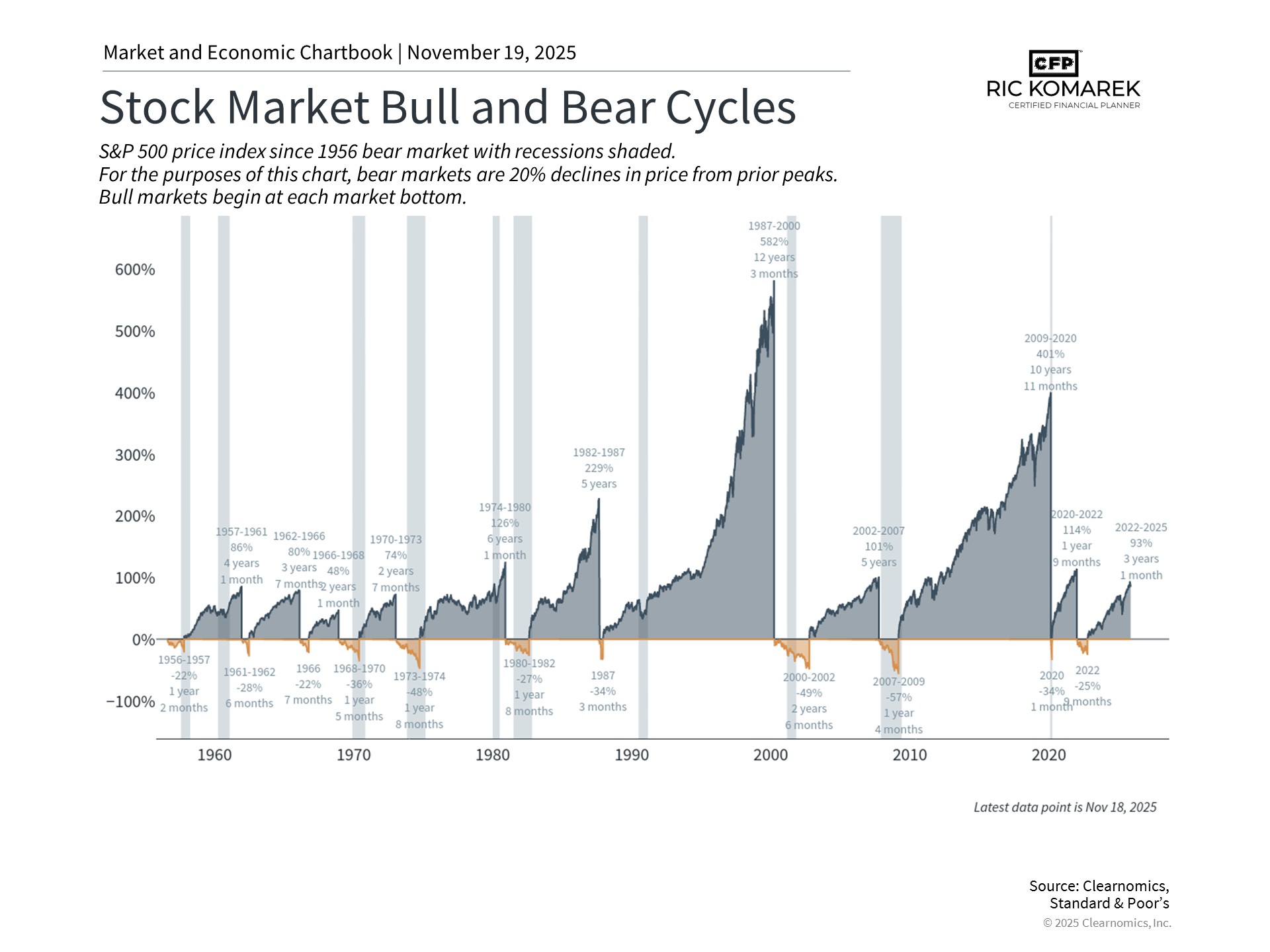

Gratitude and Growth: Putting Market Cycles in Perspective

As we gather for the holidays, it’s easy to worry about what could go wrong in the economy. But when we look at the history of market cycles, there is actually a lot to be thankful for. Here is a look... ...more

Market ,Investing

November 20, 2025•4 min read

Beyond the Headlines: A Thankful Look at Your Finances

This holiday season, let's look past the scary headlines. I'm sharing a few key reasons to be thankful for the market's performance and, more importantly, what it means for your retirement plan. ...more

Investing

November 17, 2025•5 min read

Your trusted partner in financial growth and investment success, committed to securing your financial future.